Starbucks 401(k) Login & Plan Explained Future Roast Benefits, Match, Eligibility, & After Quitting

Working at Starbucks offers more than hourly wages and employee perks. One of the most valuable benefits available to partners (employees) is the company’s Future Roast Starbucks 401(k) retirement savings plan.

This employer-sponsored retirement program allows partners to build long-term wealth through payroll contributions, employer matching, and tax advantages.

Many employees search for answers to questions like:

-

Does Starbucks offer a 401(k)?

-

How much does Starbucks match?

-

How do I log into my Starbucks retirement account?

-

What happens to my 401(k) if I leave Starbucks?

This guide explains everything you need to know about the Starbucks retirement plan from eligibility and employer match to rollover options after leaving the company.

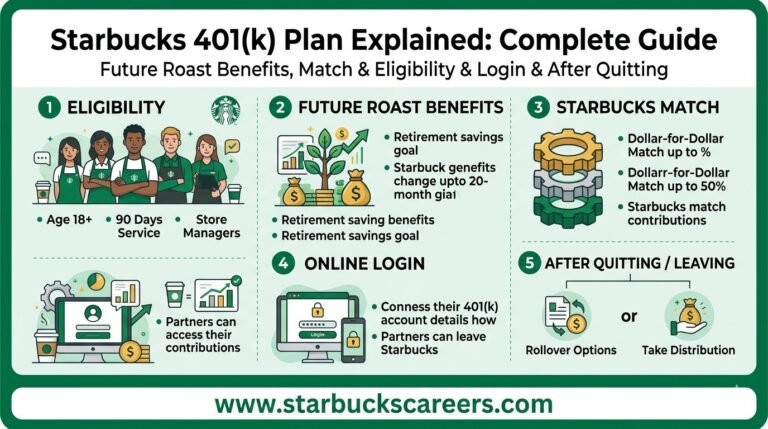

What Is the Starbucks Future Roast 401(k)?

The Future Roast 401(k) is Starbucks’ official employer-sponsored Retirement Savings Plan. It allows employees to contribute a portion of their paycheck toward retirement while receiving matching contributions from the company.

The plan follows regulations under Internal Revenue Code Section 401(k), which governs retirement savings programs in the United States.

Starbucks partners can contribute through:

-

Traditional 401(k) (tax-deferred contributions)

-

Roth 401(k) (after-tax contributions)

Accounts are administered by Fidelity Investments using the Fidelity NetBenefits platform.

Key Features of the Starbucks 401(k)

| Feature | Details |

|---|---|

| Plan Name | Future Roast 401(k) |

| Administrator | Fidelity Investments |

| Employer Match | Up to 5% of eligible pay |

| Vesting | Immediate |

| Contribution Types | Traditional & Roth |

| Investment Options | Mutual funds, target date funds, bonds |

The combination of employer contributions and tax advantages makes the plan one of the most valuable benefits available to Starbucks employees.

Why the Starbucks 401(k) Matters for Employees

A workplace retirement plan helps employees build long-term savings through automatic payroll deductions and employer matching.

For example, if an employee contributes 5% of their salary, Starbucks may contribute the same percentage.

Over time, this additional contribution compounds and significantly increases retirement savings.

Example of Long-Term Growth

| Annual Salary | Employee Contribution (5%) | Starbucks Match | Total Annual Investment |

|---|---|---|---|

| $30,000 | $1,500 | $1,500 | $3,000 |

| $40,000 | $2,000 | $2,000 | $4,000 |

| $50,000 | $2,500 | $2,500 | $5,000 |

When invested over 20–30 years, these contributions can grow substantially due to compound interest.

Starbucks 401(k) Employer Match Explained

One of the most searched questions is: How much does Starbucks match in the 401(k)?

Starbucks matches 100% of employee contributions up to 5% of eligible pay, provided eligibility requirements are met.

How the Match Works

If you contribute:

-

3% of your salary → Starbucks matches 3%

-

5% of your salary → Starbucks matches the full 5%

-

More than 5% → Starbucks still matches only up to 5%

This employer match effectively increases an employee’s compensation.

Example Scenario

A Starbucks partner earning $35,000 per year contributes 5%.

-

Employee contribution: $1,750

-

Starbucks contribution: $1,750

-

Total yearly investment: $3,500

Over a decade, this extra contribution significantly increases retirement savings.

Starbucks 401(k) Eligibility Requirements

Not every employee automatically qualifies for employer matching immediately.

To receive Starbucks 401(k) matching contributions, employees typically must:

-

Be at least 18 years old

-

Complete one year of service

-

Work 1,000 hours within that year

Once eligible, employees can begin receiving employer contributions.

Do Part-Time Employees Qualify?

Yes.

Starbucks is known for offering benefits to part-time partners, including retirement savings programs. However, the hour requirements must still be met.

Traditional vs Roth 401(k) Options

The Starbucks Future Roast plan offers two contribution types.

Traditional 401(k)

-

Contributions are pre-tax

-

Reduces taxable income today

-

Taxes paid during retirement withdrawals

Roth 401(k)

-

Contributions are after-tax

-

Withdrawals in retirement may be tax-free

-

Suitable for employees expecting higher income later

Quick Comparison

| Feature | Traditional 401(k) | Roth 401(k) |

|---|---|---|

| Tax Timing | Tax later | Tax now |

| Impact on paycheck | Lower taxable income | No immediate tax deduction |

| Best for | Higher earners | Younger workers |

Both options follow rules set by the Internal Revenue Service.

Starbucks 401(k) Vesting Schedule

Vesting determines when employees fully own employer contributions. Many companies use gradual vesting schedules that take several years. Starbucks differs.

Starbucks Vesting Policy

Employer contributions are 100% immediately vested.

This means:

-

You own all employer contributions immediately

-

Leaving the company does not forfeit your match

-

Funds remain yours even if you resign

Immediate vesting is considered generous compared to many retail employers.

Starbucks 401(k) Investment Options

The retirement account offers multiple investment choices designed for different risk levels and retirement timelines.

Common options include:

-

Target date retirement funds

-

U.S. stock index funds

-

International equity funds

-

Bond funds

-

Stable value funds

Many employees choose target date Funds, which automatically adjust the investment mix as retirement approaches.

Example Portfolio Strategy

A younger employee might invest heavily in stock funds for growth, while an employee closer to retirement may choose a balanced mix of stocks and bonds.

How to Log Into Your Starbucks 401(k)

Starbucks retirement accounts are accessed through Fidelity NetBenefits.

Steps to Access Your Account

-

Visit the Fidelity NetBenefits website

-

Enter your username and password

-

Select the Starbucks Future Roast plan

-

View your retirement dashboard

Once logged in, employees can:

-

Check their account balance

-

Adjust contribution percentages

-

Select investment funds

-

Download statements

-

Update beneficiary information

If login problems occur, employees can reset credentials or contact Fidelity support.

Contribution Limits for the Starbucks 401(k)

The amount employees can contribute each year is limited by federal regulations.

The Internal Revenue Service sets annual contribution limits.

Typical contribution ranges include:

-

Employee contribution limits in the $20,000+ range annually

-

Additional catch-up contributions for workers over 50

Employer matching contributions do not count toward the employee contribution limit.

What Happens to Your Starbucks 401(k) After Quitting?

Many employees worry about losing retirement savings when they leave the company.

Fortunately, that is not the case.

Because Starbucks uses immediate vesting, employees keep:

-

Their own contributions

-

All employer matching contributions

-

Any investment growth

The retirement account remains yours even after leaving the company.

Your Options After Leaving Starbucks

When leaving Starbucks, employees generally have four choices for their 401(k).

Option 1: Leave the Account With Fidelity

You can keep your retirement funds in the existing account managed by Fidelity Investments.

Advantages:

-

No paperwork required

-

Investments remain unchanged

Option 2: Roll Over to an IRA

Many former employees transfer funds into an Individual Retirement Account.

Benefits include:

-

More investment choices

-

Consolidating multiple retirement accounts

-

Potentially lower fees

Option 3: Transfer to a New Employer’s 401(k)

If your new employer offers a retirement plan, you may transfer the balance into the new account.

Advantages:

-

Simplifies retirement planning

-

Keeps funds tax-deferred

Option 4: Withdraw the Money

You can withdraw funds, but this option often has drawbacks.

Possible consequences:

-

Income taxes

-

Early withdrawal penalties if under age 59½

Because of these penalties, financial advisors typically recommend rollovers instead.

Starbucks 401(k) vs IRA: Which Is Better?

Employees often compare employer plans with personal retirement accounts.

Comparison Table

| Feature | Starbucks 401(k) | IRA |

|---|---|---|

| Employer match | Yes | No |

| Investment options | Limited | Broad |

| Contribution limits | Higher | Lower |

| Ease of use | Automatic payroll deductions | Self-managed |

Many employees use both accounts for a diversified retirement strategy.

Retirement Planning Tips for Starbucks Employees

Employees can maximize their retirement savings by following a few key practices.

Contribute at Least 5%

This ensures you receive the full employer match.

Increase Contributions Gradually

Increasing contributions by just 1% each year can significantly grow retirement savings.

Diversify Investments

Avoid placing all contributions in a single fund. A balanced portfolio can reduce long-term risk.

Avoid Early Withdrawals

Taking money out early reduces long-term compound growth.

Starbucks Retirement Benefits in Canada

In Canada, retirement plans differ from the United States. Instead of a 401(k), employees may have access to a group retirement savings plan similar to an RRSP.

Key differences include:

-

Contributions structured under Canadian retirement regulations

-

Tax treatment based on Canadian law

-

Employer matching policies may vary

Canadian partners should review plan details through Starbucks benefits portals or HR resources.

Starbucks Employee Pension in the United Kingdom

Employees in the United Kingdom typically participate in a workplace pension scheme rather than a 401(k).

Features may include:

-

Automatic enrollment

-

Employer pension contributions

-

Tax advantages under UK pension regulations

Specific contribution rates may differ depending on employment status and government pension rules.

Common Mistakes Starbucks Employees Make With Their 401(k)

Even when employees have access to retirement benefits, common mistakes can limit their savings potential.

Contributing Too Little

Failing to contribute at least 5% means missing out on free employer matching.

Cashing Out After Leaving

Withdrawing funds early can trigger:

-

Income taxes

-

Early withdrawal penalties

Ignoring Investment Choices

Leaving funds in low-growth investments may reduce long-term returns.

Not Updating Beneficiaries

Employees should periodically review beneficiary designations to ensure retirement funds go to the correct person.

Conclusion

The Starbucks Future Roast 401(k) is one of the most valuable benefits available to Starbucks Partners. Through payroll contributions, employer matching, and tax advantages, the plan helps employees build long-term Financial Security.

By contributing at least enough to receive the full employer match and making thoughtful investment choices, employees can significantly increase their retirement savings.

Understanding your options especially when leaving the company ensures you avoid unnecessary taxes and penalties while keeping your retirement plan on track.

FAQs

Does Starbucks offer a 401(k) plan?

Yes. Starbucks offers the Future Roast 401(k) retirement plan, allowing partners to contribute pre-tax or Roth savings while receiving employer matching contributions.

How much does Starbucks match in the 401(k)?

Starbucks matches 100% of employee contributions up to 5% of eligible pay once eligibility requirements are met.

How long must you work at Starbucks to get the 401(k) match?

Employees must generally complete one year of service and 1,000 hours worked before becoming eligible for the employer match.

Is the Starbucks 401(k) immediately vested?

Yes. Employer contributions are 100% immediately vested, meaning employees own the funds right away.

Can part-time Starbucks employees get a 401(k)?

Yes. Both part-time and full-time Starbucks partners may participate in the retirement plan if they meet the eligibility requirements.

Who manages Starbucks retirement accounts?

Starbucks retirement plans are administered by Fidelity Investments, and employees manage their accounts through Fidelity NetBenefits.

What happens to my Starbucks 401(k) if I quit?

You keep all contributions and employer matches. You can leave the account with Fidelity, roll it into an IRA, transfer it to a new employer’s plan, or withdraw funds.

Can I withdraw my Starbucks 401(k) early?

Yes, but withdrawals before age 59½ may result in taxes and a 10% early withdrawal penalty.

What investment options are available in the Starbucks 401(k)?

Investment choices typically include target date funds, stock index funds, international funds, and bond funds.

How do I log into my Starbucks 401(k)?

Employees access their retirement accounts through the Fidelity NetBenefits website, where they can manage contributions, investments, and account details.

Do Starbucks employees in Canada or the UK have a 401(k)?

No. Employees in Canada and the United Kingdom usually participate in different retirement savings plans, such as RRSP-style plans in Canada or workplace pensions in the UK.

Should I roll over my Starbucks 401(k) after leaving?

Many employees choose to roll their balance into an Individual Retirement Account (IRA) or transfer it to a new employer’s retirement plan to avoid taxes and maintain tax-deferred growth.